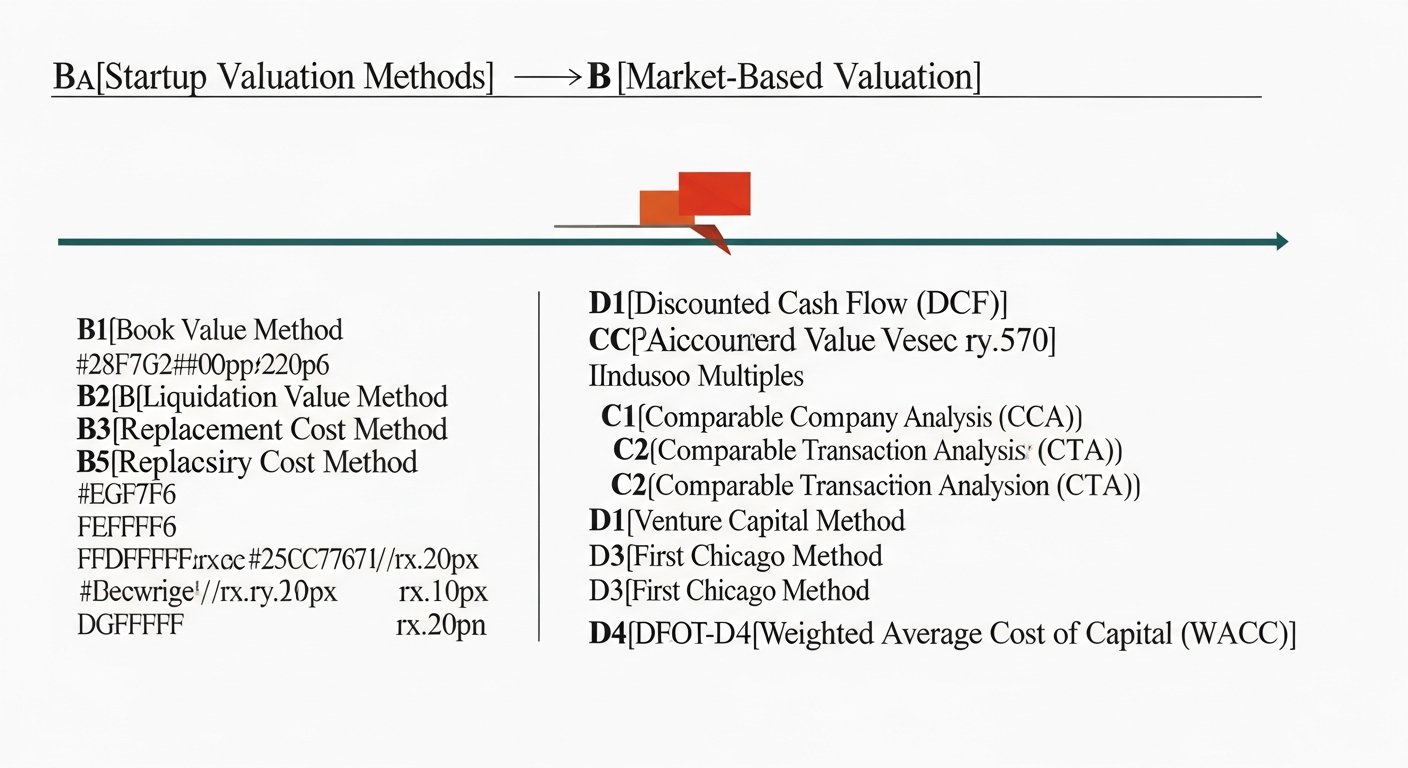

What Are Startup Valuation Methods for Tech Ventures and Why Do They Matter?

|

For any entity operating within the dynamic realm of Tech Startup Growth & Management, understanding startup valuation methods is not merely an academic exercise; it is a critical skill. These systematic approaches to determining a tech startup’s economic worth are foundational for navigating the complex journey from ideation to exit. Valuation is paramount for securing essential funding, negotiating equitable shares for founders and early employees, facilitating strategic planning, and fostering robust investor relations. Given the unique characteristics of tech ventures—rapid innovation, high growth potential, often limited tangible assets, and significant risk factors—traditional valuation models frequently fall short. Consequently, a diverse array of specialized methods has emerged, each tailored to different stages of a tech startup’s lifecycle and the specific attributes it possesses, from its nascent, pre-revenue days to its mature, post-revenue scaling phases. This article will delve into these essential valuation methodologies, exploring their application, benefits, and drawbacks to equip founders, investors, and stakeholders with the knowledge needed to thrive in the competitive tech landscape.

Startup valuation methods are structured frameworks used to estimate the monetary value of a private company, particularly those in their early stages of development. Unlike publicly traded companies with readily available market data, tech startups require bespoke approaches that can account for their unique blend of immense future potential and inherent uncertainty. The primary objective is to arrive at a fair price that satisfies both the startup seeking capital and investors providing it, ensuring a foundation for sustainable Tech Startup Growth & Management. Demystify these crucial techniques for tech ventures, covering early-stage, growth-stage, and advanced strategies to secure funding and manage equity effectively.

What Are Early-Stage Startup Valuation Methods for Navigating Uncertainty?

For tech startups in their nascent, often pre-revenue stages, traditional financial models fall short. They lack historical data, predictable cash flows, and established market comparables. This section delves into startup valuation methods specifically designed to assess potential, team, and market opportunity, crucial for securing seed funding and laying the groundwork for growth management. These methods prioritize qualitative factors and forward-looking projections over past performance.

What is The Scorecard Method for Benchmarking Potential?

The Scorecard Method, developed by Christopher Mirabile of the Angel Capital Association, is a popular qualitative approach for valuing early-stage tech startups. This method compares the target startup to other funded startups in the same region and industry, then adjusts the average valuation based on a series of qualitative factors.

- Core Definition: A comparative method that evaluates a startup against a benchmark of recently funded similar companies, adjusting for relative strengths and weaknesses.

- Underlying Principles: Recognizes that early-stage valuation is subjective and relies heavily on an assessment of key qualitative drivers of success.

- Key Inputs/Data Required:

- Average pre-money valuation of comparable startups in the region/sector.

- Qualitative assessment factors:

- Strength of the Management Team (0-30%)

- Size of the Opportunity (0-25%)

- Product/Technology (0-15%)

- Competitive Environment (0-10%)

- Marketing/Sales Channels (0-10%)

- Need for Additional Investment (0-5%)

- Advantages:

- Accounts for crucial qualitative aspects often overlooked by quantitative methods.

- Relatively simple to apply for pre-revenue startups with limited financial data.

- Provides a structured way to justify a valuation to angel investors.

- Disadvantages:

- Highly subjective; results can vary depending on the assessor.

- Requires access to reliable comparable deal data, which can be challenging.

- Doesn’t directly predict future financial performance.

- Specific Scenarios/Types of Tech Startups: Ideal for seed-stage, pre-revenue SaaS companies or hardware startups needing initial capital, where the team and market potential are primary drivers.

How is the Berkus Method Applied for Pre-Revenue Startups?

The Berkus Method, conceived by super angel investor Dave Berkus, is another quick and intuitive approach for valuing pre-revenue startups. It assigns a monetary value to specific risk-reduction milestones rather than projecting future earnings.

- Core Definition: A qualitative method that assigns a maximum value of $500,000 for five key risk-reduction elements, leading to a maximum pre-money valuation of $2.5 million.

- Underlying Principles: Focuses on the idea that investors value progress in mitigating fundamental risks inherent in early-stage ventures.

- Simplified Formula: Sum of assigned values for each of the following (up to $500K each):

- Sound Idea (Basic Value)

- Prototype (Reduces Technology Risk)

- Quality Management Team (Reduces Execution Risk)

- Strategic Relationships (Reduces Market Risk)

- Product Rollout/Initial Sales (Reduces Production/Market Risk)

- Key Inputs/Data Required: Qualitative assessment of the startup’s progress against the five key milestones.

- Advantages:

- Extremely simple and fast to apply.

- Focuses on value drivers relevant to early-stage tech startups before revenue generation.

- Provides a reasonable “gut check” valuation for angel investors.

- Disadvantages:

- Highly subjective; ignores market dynamics and competitive landscape.

- Caps the valuation, potentially underestimating truly disruptive innovations.

- Lacks financial rigor for later funding rounds or larger investments.

- Specific Scenarios/Types of Tech Startups: Best suited for pre-seed and seed-stage tech startups seeking initial funding from individual investors or accelerators, particularly for ventures with strong founding teams and compelling ideas.

What is the Venture Capital Method for Investor-Centric Valuation?

The Venture Capital (VC) Method is widely used by VCs to determine investment terms. It works backward from a projected exit valuation to calculate the current pre-money valuation, considering the desired return on investment (ROI).

- Core Definition: Projects the startup’s value at a future exit event, then discounts that value back to the present based on the VC’s required rate of return.

- Underlying Principles: VCs invest with the expectation of a significant multiple return on their capital within a specific timeframe (e.g., 5-7 years). The method calculates the initial equity stake needed to achieve this.

- Simplified Formula:

Post-Money Valuation = Exit Value / Desired ROI Multiple

Pre-Money Valuation = Post-Money Valuation – Investment Amount

Investor Ownership % = Investment Amount / Post-Money Valuation

- Key Inputs/Data Required:

- Projected Exit Value (e.g., based on market multiples of revenue or EBITDA at exit).

- Desired ROI (typically 5x to 10x or higher for early-stage investments).

- Investment Amount required.

- Advantages:

- Aligns with the forward-looking, exit-driven strategy of venture capitalists.

- Incorporates the significant dilution that often occurs in subsequent funding rounds.

- Provides a clear framework for negotiating ownership stakes.

- Disadvantages:

- Relies heavily on accurate predictions of future exit value and timing, which are highly uncertain for early-stage companies.

- The high desired ROI can lead to lower initial valuations for the founders.

- Can sometimes overlook the intrinsic value of the company in favor of investor returns.

- Specific Scenarios/Types of Tech Startups: Essential for early-stage tech startups seeking significant capital from institutional venture capitalists, especially those with high growth potential targeting large market opportunities.

What Are Growth-Stage Startup Valuation Methods for Assessing Scalable Potential?

As tech startups mature and begin generating revenue, the valuation landscape shifts. With more robust financial data and a clearer market position, more quantitative and data-driven startup valuation methods become applicable. This section explores methodologies suitable for assessing measurable performance and scalable potential, critical for sustained growth management and attracting larger investments.

How is Discounted Cash Flow (DCF) Used for Revenue-Generating Tech Startups?

The Discounted Cash Flow (DCF) method is a cornerstone of financial valuation, highly regarded for its fundamental approach. It determines a company’s value based on its projected future cash flows, discounted back to their present value.

- Core Definition: Values a company by estimating its future free cash flows and discounting them back to the present using a discount rate that reflects the risk and cost of capital.

- Underlying Principles: The intrinsic value of a business is the present value of its expected future cash flows.

- Simplified Formula:

PV = Σ [CFt / (1 + r)t] + TV / (1 + r)n

Where:

- PV = Present Value

- CFt = Free Cash Flow in year t

- r = Discount Rate (WACC – Weighted Average Cost of Capital)

- t = Year number

- TV = Terminal Value (value of cash flows beyond the explicit forecast period)

- n = Number of years in the explicit forecast period

- Key Inputs/Data Required:

- Detailed financial projections (revenue, expenses, capital expenditures, working capital).

- Free Cash Flow (FCF) calculations.

- A robust discount rate (WACC or similar, reflecting cost of equity and debt).

- Assumptions for terminal value (e.g., perpetuity growth model, exit multiple).

- Sensitivity analysis for key variables.

- Advantages:

- Considered a fundamental and theoretically sound method.

- Provides an intrinsic value, less influenced by market sentiment fluctuations.

- Excellent for post-revenue SaaS companies or hardware startups with clear product roadmaps and predictable recurring revenue (ARR/MRR).

- Allows for scenario planning and growth potential analysis.

- Disadvantages:

- Highly sensitive to assumptions, particularly future cash flow projections and the discount rate.

- Difficult to apply accurately for companies with highly uncertain future cash flows.

- Requires significant historical data and sophisticated financial modeling expertise.

- Specific Scenarios/Types of Tech Startups: Best for growth-stage tech startups with established revenue streams, a clear business model, and reasonable predictability in their financial forecasts.

What is Comparable Company Analysis (CCA) for Market-Based Insights?

Comparable Company Analysis (CCA), also known as “Comps,” is a relative valuation method that assesses a company’s value by comparing it to similar businesses that have recently been sold or are publicly traded.

- Core Definition: Values a company by comparing its key financial metrics and operating characteristics to those of similar publicly traded companies or recently acquired private companies.

- Underlying Principles: Market efficiency suggests that similar assets should trade at similar prices.

- Key Metrics/Data Points:

- Revenue Multiples (e.g., Enterprise Value / Revenue, EV/SaaS ARR)

- EBITDA Multiples (e.g., EV/EBITDA)

- User-based Multiples (e.g., EV/Active Users for social media/gaming platforms)

- Industry-specific metrics (e.g., Customer Acquisition Cost, LTV)

- Growth rates, profitability, market size, business model.

- Advantages:

- Reflects current market sentiment and investor appetite for similar assets.

- Relatively straightforward to apply if robust comparables are available.

- Useful for justifying a valuation in funding rounds by referencing market precedents.

- Disadvantages:

- Finding truly comparable private tech startups can be challenging due to data scarcity.

- Market sentiment can lead to over or undervaluation.

- Difficult to adjust for unique attributes or competitive advantages of the target company.

- Less relevant for highly unique or disruptive business models without clear parallels.

- Specific Scenarios/Types of Tech Startups: Suitable for growth-stage tech startups in established sub-sectors (e.g., FinTech, EdTech, specific SaaS niches) where public or private transaction comparables are accessible.

When is Asset-Based Valuation Relevant for Tech?

Asset-based valuation calculates a company’s value based on the fair market value of its tangible and intangible assets, minus its liabilities. While less common for typical tech startups, it has niche applications.

- Core Definition: Determines a company’s value by summing the fair market value of all its assets and subtracting its liabilities.

- Underlying Principles: A company is worth at least the sum of its parts.

- Key Inputs/Data Required:

- Fair market value of tangible assets (cash, equipment, real estate).

- Fair market value of intangible assets (intellectual property portfolio, patents, trademarks, software code, customer lists).

- Total liabilities.

- Advantages:

- Provides a baseline “floor” valuation, particularly for companies with significant tangible assets or highly valuable, defensible IP.

- Useful for liquidation scenarios or distressed companies.

- Can be a component of due diligence for startups with substantial IP.

- Disadvantages:

- Often undervalues typical tech startups where future growth and intangible potential are primary drivers.

- Difficult to accurately value many intangible tech assets (e.g., proprietary algorithms, user data).

- Doesn’t account for ongoing operations, future earnings, or growth potential.

- Specific Scenarios/Types of Tech Startups: Rarely the primary method for high-growth tech. More relevant for hardware manufacturing startups with significant physical assets, startups with a strong patent portfolio, or in cases of potential bankruptcy or acquisition where the buyer is primarily interested in specific assets.

What Are Advanced & Strategic Valuation Considerations for Tech Startups?

Beyond the quantitative aspects of valuation methods, understanding their strategic implications is crucial for sophisticated tech startup growth and management. This involves considering the value of flexibility, the impact of equity incentives, and other nuanced factors that can significantly influence a startup’s perceived worth and future trajectory.

What is Real Options Valuation and How Does it Value Flexibility?

Traditional valuation methods often struggle to capture the value of managerial flexibility and strategic choices inherent in many tech ventures. Real Options Valuation (ROV) attempts to address this by applying options pricing theory to real assets and strategic decisions.

- Core Definition: A valuation approach that considers the value of management’s ability to make future decisions (e.g., expand, defer, abandon a project) in response to changing market conditions.

- Underlying Principles: Many strategic investments in tech are analogous to financial options, where the company has the right, but not the obligation, to pursue future opportunities.

- Advantages:

- Captures the value of flexibility and strategic choices, which is highly relevant for tech startups operating in uncertain environments.

- Better reflects the true value of R&D investments or platform strategies that unlock future opportunities.

- Can provide a more comprehensive picture for ventures with high risk factors but significant upside potential.

- Disadvantages:

- Highly complex and requires specialized financial modeling expertise.

- Difficult to identify and quantify “real options” in practice.

- Not widely accepted or understood by all investors.

- Specific Scenarios/Types of Tech Startups: Most applicable for tech startups developing platform technologies, engaging in significant R&D, or having potential for multiple future strategic pivots (e.g., biotech, advanced AI, deep tech) where the value of deferring or expanding investments is substantial.

How Do Option Pools and ESOPs Impact Startup Valuation?

Employee Stock Option Plans (ESOPs) and the creation of option pools are standard practices in tech startup growth and management, crucial for attracting and retaining top talent. However, they have a direct and often significant impact on startup valuation and founder dilution.

- Option Pool Definition: A reserve of company stock (typically 10-20% of total shares) set aside for future grants to employees, advisors, and potentially board members.

- Pre-Money vs. Post-Money Impact:

- Pre-money valuation discussions often involve negotiating the size of the option pool. Investors typically prefer the option pool to be “pre-money,” meaning its dilution effect is borne by the existing shareholders (founders) before their investment.

- If the option pool is created “post-money,” the investor also shares in the dilution.

- The larger the option pool created pre-money, the lower the effective pre-money valuation for existing shareholders, leading to increased founder dilution.

- Investor Expectations: Investors typically expect a reasonable option pool to be in place or created before their investment, recognizing its importance for future hiring and motivation. This is a common point of negotiation in term sheets.

- Equity Management: Strategic management of the option pool is essential to balance talent acquisition needs with minimizing unnecessary dilution and preserving founder and early investor stakes.

How to Choose the Right Startup Valuation Method for Your Tech Startup?

Selecting the appropriate startup valuation method is a strategic decision that can significantly influence funding outcomes and the overall trajectory of tech startup growth and management. There’s no single “best” method; rather, the choice depends on a confluence of factors unique to each venture.

What Key Factors Influence Startup Valuation Method Selection?

When approaching valuation, founders and investors should consider the following critical elements:

- Startup Stage: This is arguably the most crucial factor.

- Pre-Seed/Seed-Stage (Idea/Prototype): Methods like Scorecard, Berkus, and VC Method are preferred due to limited financial data and focus on qualitative factors (team, market, idea).

- Early Growth (Initial Revenue): A blend of early-stage methods and the nascent application of DCF or CCA might be used, often with high discount rates or significant adjustments.

- Growth Stage (Scaling Revenue): DCF and CCA become primary, backed by more reliable financial projections and market comparables.

- Mature/Pre-Exit: Sophisticated DCF models, detailed CCA, and potentially LBO (Leveraged Buyout) analyses become relevant.

- Data Availability: The quantity and quality of historical financial data, market research, and comparable company information will dictate which methods are feasible. Pre-revenue startups have less data, necessitating methods less reliant on financials.

- Industry & Business Model:

- SaaS companies with predictable recurring revenue (ARR/MRR) are well-suited for DCF and revenue multiples in CCA.

- Marketplace businesses might use user growth metrics or transaction volume multiples.

- Deep tech/biotech with long R&D cycles might benefit from Real Options Valuation.

- Purpose of Valuation:

- Seeking Seed Funding: Often more qualitative methods or VC Method.

- Series A/B Funding: A combination of DCF and CCA, with increasing rigor.

- M&A / Exit: Comprehensive DCF, CCA, and possibly precedent transactions.

- Employee Stock Options: Simpler, consistent methods for internal purposes.

- Type of Investor:

- Angel Investors: Often comfortable with simpler, qualitative methods.

- Venture Capitalists: Heavily rely on the VC Method, often coupled with DCF and CCA.

- Strategic Investors: May have unique valuation perspectives based on synergy.

- Total Addressable Market (TAM) & Competitive Landscape: A large TAM and a strong competitive moat can justify higher valuations, which valuation methods need to capture through growth assumptions.

- Management Team Experience: The track record and expertise of the founders and management team are significant qualitative factors influencing investor confidence and valuation, particularly in early stages.

When Should You Seek Professional Valuation Expertise?

While founders can gain a foundational understanding of valuation, certain situations necessitate engaging professional valuators or investment bankers:

- Complex Funding Rounds: For Series A and beyond, particularly with multiple investors, complex cap tables, or unique investment instruments (e.g., convertible notes, SAFEs with caps/discounts).

- Mergers & Acquisitions (M&A): When preparing for an acquisition or being acquired, an independent valuation provides credibility and helps negotiate fair terms.

- Strategic Partnerships or Joint Ventures: To determine fair equity splits or contributions.

- Litigation or Dispute Resolution: For legal purposes, a certified valuation is often required.

- IPO Preparation: Rigorous valuation is paramount before going public.

- High Stakes Negotiations: When significant capital is at stake, an expert opinion can strengthen a startup’s negotiating position and identify potential hidden values or risks.

What is the Role of Valuation in Tech Startup Funding Rounds & Equity Management?

Valuation is the central pillar around which all tech startup funding rounds revolve. It directly dictates how much equity an investor receives for their capital and, consequently, the level of dilution experienced by existing shareholders, including the founders. Effective equity management is therefore intrinsically linked to a clear understanding of valuation.

Understanding Pre-Money and Post-Money Valuation

- Pre-Money Valuation: This is the value of the company *before* a new investment. It represents what the existing shareholders (founders, early employees, previous investors) own.

- Post-Money Valuation: This is the value of the company *after* a new investment. It equals the pre-money valuation plus the new investment amount.

- Example: If a startup has a $10 million pre-money valuation and raises $2 million, its post-money valuation is $12 million. The new investor gets 2/12 (16.67%) of the company.

How Does Valuation Impact Funding Rounds and Dilution?

Each subsequent funding round (Seed, Series A, Series B, etc.) involves a new valuation, which determines the share price for that round. Higher valuations generally mean less dilution for existing shareholders, as the same amount of capital buys a smaller percentage of the company.

- Seed Stage: Often relies on qualitative methods. Valuations can be lower, leading to higher initial dilution for founders, but this is often necessary to get the venture off the ground. Convertible notes and SAFEs are common in this stage, deferring valuation to a later equity round.

- Series A & Beyond: Valuations become more sophisticated, using DCF, CCA, and robust financial modeling. Investors, including venture capitalists, carefully scrutinize valuation to ensure their desired ROI and mitigate risk factors. Each round inevitably brings further dilution, but successful growth should ensure the value of the remaining equity increases.

How Does Valuation Affect Equity Distribution and Investor Expectations?

Valuation directly impacts the distribution of equity among various stakeholders:

- Founders: Valuation determines their initial equity stake and how much they are diluted in subsequent rounds. Maintaining a significant ownership stake while raising capital is a key challenge in Tech Startup Growth & Management.

- Employees: Employee stock options (ESOPs) are granted at the current fair market value, incentivizing them with potential future gains. A clear valuation framework helps define these grants.

- Angel Investors & Venture Capitalists: Their investment thesis is built around a specific valuation that allows for their target returns. A lower valuation means more equity for their money, which is why valuations are intensely negotiated in term sheets.

- Board of Directors & Advisors: May receive equity grants, which are also tied to the company’s valuation.

Understanding the interplay between valuation, funding amounts, and equity percentages is crucial for transparent communication with all stakeholders and for building a sustainable equity management strategy.

What Are Common Pitfalls and Best Practices in Tech Startup Valuation?

Navigating startup valuation methods without succumbing to common errors is vital for sound Tech Startup Growth & Management. Both founders and investors can make mistakes that lead to suboptimal outcomes. Understanding these pitfalls and adhering to best practices can significantly improve negotiation outcomes and long-term success.

What Are Common Pitfalls in Startup Valuation?

- Overvaluation:

- Consequences: Can make it difficult to raise subsequent funding rounds (a “down round” which signals distress), demoralize employees whose options are underwater, deter future investors seeking higher returns, and lead to unrealistic expectations.

- Causes: Unrealistic projections, emotional attachment to the company, incorrect comparable selection, ignoring dilution effects, or accepting overly optimistic terms in early rounds.

- Undervaluation:

- Consequences: Founders give away too much equity too early, leading to excessive founder dilution and potentially losing control or significant wealth. It can also signal a lack of confidence.

- Causes: Lack of understanding of market value, desperation for funding, poor negotiation skills, or underestimating the company’s true growth potential and intellectual property value.

- Incorrect Comparable Selection: Using companies that are not truly similar in stage, industry, business model, or geography can lead to skewed valuations, either too high or too low.

- Ignoring Dilution: Founders often overlook the cumulative impact of dilution across multiple funding rounds, not realizing how much their ownership percentage will shrink over time.

- Unrealistic Projections: Overly aggressive revenue forecasts or underestimating expenses can inflate DCF models, leading to an artificially high valuation that fails to materialize.

- Focusing on a Single Method: Relying solely on one valuation method (e.g., just the Berkus Method) without cross-referencing with others can provide a very narrow and potentially inaccurate picture.

- Lack of Transparency: Hiding crucial information or presenting biased data to investors can erode trust and jeopardize deals.

- Not Factoring in Option Pools: Failing to properly account for the impact of employee option pools on pre-money valuation can lead to unexpected dilution.

What Are Best Practices in Tech Startup Valuation?

- Embrace Data Integrity & Transparency: Ensure all financial data, projections, and assumptions are accurate, well-documented, and defensible. Be transparent with investors, even about challenges.

- Utilize Multiple Valuation Methods: Employ a range of relevant methods (e.g., Scorecard + VC Method for early-stage; DCF + CCA for growth-stage) to establish a valuation range. This triangulation provides a more robust and defensible figure.

- Understand Investor Perspective: Step into the shoes of potential investors. What are their desired ROI? What risk factors are they assessing? How do they view your growth potential against their portfolio?

- Benchmark Against Industry Norms: Research valuation multiples and deal terms for similar companies in your sector and stage. Tools like PitchBook or Crunchbase can be invaluable.

- Build Defensible Financial Models: For DCF, ensure your financial model is robust, flexible, and clearly articulates assumptions. Perform sensitivity analysis to show how valuation changes under different scenarios.

- Prioritize Team & IP in Early Stages: For pre-revenue startups, emphasize the strength of your management team experience, the defensibility of your intellectual property portfolio, and the size of your total addressable market (TAM).

- Account for Dilution Strategically: Plan for future dilution. Understand how current investment terms will impact your equity over time. Manage your option pool judiciously.

- Seek Professional Advice: Engage experienced startup advisors, lawyers, and financial consultants for complex valuations or critical funding rounds. Their expertise can be invaluable in avoiding costly mistakes.

- Maintain Open Communication: Foster a relationship of trust with investors through clear and consistent communication about performance, challenges, and strategic direction.

| Valuation Method | Best For (Startup Stage/Type) | Key Inputs/Data | Pros | Cons | Example Tech Startup Application |

|---|---|---|---|---|---|

| Scorecard Method | Pre-Seed/Seed, Pre-Revenue | Comparable valuations, qualitative factors (team, market, product) | Considers qualitative factors; relatively simple | Subjective; requires comparable data; not financially rigorous | Early-stage SaaS with strong team but no revenue yet |

| Berkus Method | Pre-Seed/Seed, Pre-Revenue | Assessment of 5 risk-reduction milestones | Extremely simple; quick “gut check” for angel investors | Highly subjective; capped valuation; ignores market | An innovative mobile app concept with a working prototype |

| Venture Capital Method | Seed/Series A, High Growth Potential | Projected exit value, desired ROI, investment amount | Aligns with VC exit strategy; accounts for dilution | Relies on uncertain exit value; can lead to low pre-money | Biotech startup seeking large Series A for drug development |

| Cost-to-Duplicate Method | Specific IP/Asset-Heavy, or Distressed Assets | Cost to build current product/IP from scratch | Provides a floor value; objective for tangible assets | Ignores future growth/market; undervalues true potential | Deep tech with highly specialized, defensible hardware or software, or a startup selling its assets. |

| Valuation Method | Best For (Startup Stage/Type) | Key Metrics/Data Points | Pros | Cons | Example Tech Startup Application |

|---|---|---|---|---|---|

| Discounted Cash Flow (DCF) | Growth-Stage/Mature, Post-Revenue | Projected free cash flows, discount rate (WACC), terminal value | Theoretically sound; intrinsic value; robust for predictable revenue | Highly sensitive to assumptions; complex; requires detailed forecasts | Established B2B SaaS company with predictable subscription revenue |

| Comparable Company Analysis (CCA) | Growth-Stage, Post-Revenue | Revenue multiples, EBITDA multiples, user metrics of peers | Reflects market sentiment; straightforward if comparables exist | Finding true comparables is hard; susceptible to market fluctuations | FinTech platform with clear revenue and growth metrics |

| Asset-Based Valuation | Hardware/IP-Heavy, Distressed | Fair market value of tangible and intangible assets minus liabilities | Provides a floor value; objective for physical assets | Often undervalues tech companies; ignores growth potential | Hardware startup with significant manufacturing assets or a company primarily valued for its patent portfolio |

| Tech Startup Stage | Key Characteristics | Recommended Valuation Methods | Rationale |

|---|---|---|---|

| Pre-Seed/Idea | Concept, founding team, no product/revenue, high risk | Berkus Method, Scorecard Method | Focus on qualitative factors and risk reduction due to minimal data. |

| Seed Stage | Prototype/MVP, early users, limited/no revenue, strong team | Scorecard Method, Venture Capital Method, Cost-to-Duplicate | Assessing team, market, and potential with investor ROI focus. |

| Series A/Growth Stage | Established product, growing revenue (ARR/MRR), market traction, scaling operations | Discounted Cash Flow (DCF), Comparable Company Analysis (CCA), Venture Capital Method | More reliance on financial performance, market multiples, and detailed projections. |

| Mature/Pre-Exit | Significant revenue, profitability, established market, preparing for M&A or IPO | DCF, CCA, Precedent Transactions Analysis, LBO Analysis | Comprehensive financial modeling and market-based approaches become standard. |

Conclusion

Mastering startup valuation methods is an indispensable skill for anyone involved in Tech Startup Growth & Management. From the qualitative assessments crucial for pre-revenue startups navigating initial uncertainty to the sophisticated financial modeling required for growth-stage tech companies, each method offers unique insights into a venture’s economic worth. Founders, angel investors, and venture capitalists must collectively understand these tools to foster equitable partnerships, secure necessary capital, and manage equity effectively through various funding rounds.

The journey of a tech startup is characterized by rapid evolution and inherent risk. Consequently, valuation is not a static calculation but an iterative process, adapting as the company achieves milestones, gathers data, and confronts market shifts. By diligently applying the appropriate methods, understanding their nuances, avoiding common pitfalls, and embracing best practices, stakeholders can make informed decisions that pave the way for sustainable growth, successful strategic exits, and the enduring prosperity of the tech ecosystem. Ultimately, a deep comprehension of valuation methodologies transforms what could be a contentious negotiation into a strategic dialogue, aligning expectations and catalyzing the next wave of innovation.