Understanding the Core: What Exactly is Venture Capital?

At its heart, venture capital (VC) is a form of private equity financing that is provided by venture capital firms or funds to early-stage, high-potential, and high-growth companies. These are typically startups that have demonstrated a strong business model, innovative technology, or a disruptive approach to an existing market, but lack the operating history or assets to secure traditional bank loans or public market financing. Unlike conventional lenders who seek collateral and predictable returns, venture capitalists are risk-takers. They invest in companies with the potential for exponential growth and, consequently, significant returns on their investment, often over a medium to long-term horizon.

The fundamental premise of venture capital revolves around identifying and nurturing disruptive innovation. VCs are not just providing capital; they are often offering strategic guidance, operational expertise, and invaluable connections that can transform a promising startup into an industry behemoth. This hands-on approach differentiates venture capital from other forms of investment, making it a critical lifeline for many tech startups and ambitious ventures looking to scale rapidly. For instance, a startup developing cutting-edge AI for personalized learning or a new platform for sustainable energy management might find traditional banks hesitant, but a VC firm might see immense future value.

The capital provided by VCs is typically exchanged for an equity stake in the company. This means that venture capitalists become part-owners, sharing in the future successes (and failures) of the startup. This equity position aligns their interests with those of the founders: both parties are incentivized to see the company grow and eventually achieve a significant “exit event,” such as an acquisition by a larger company or an initial public offering (IPO). The high-risk nature of these investments is balanced by the potential for exceptionally high returns. While many startup investments may not pan out, the few that succeed spectacularly can more than compensate for the losses, making venture capital a lucrative, albeit challenging, asset class.

Understanding what venture capital is also involves distinguishing it from other types of funding. Angel investors, for example, are typically high-net-worth individuals who invest their own money, often at the very earliest stages, and may be less structured or formal than VC firms. Private equity, while similar, generally focuses on more mature companies, often with established cash flows, aiming to optimize operations or consolidate industries. Venture capital, specifically, targets the frontier of innovation, betting on untested ideas and unproven teams to create the next generation of market leaders. This unique focus is what makes understanding venture capital crucial for any founder aiming for significant scale and disruption.

The Key Players in the VC Ecosystem

The venture capital landscape is a complex web of interconnected entities, each playing a crucial role in funneling capital from its source to innovative startups. Understanding these players is essential for any entrepreneur seeking VC funding, as well as for anyone looking to comprehend how venture capital works. This ecosystem is broadly divided into capital providers, capital managers, and the beneficiaries of this capital.

Limited Partners (LPs): The Capital Providers

At the top of the financial food chain are the Limited Partners (LPs). These are the institutions and wealthy individuals who commit capital to venture capital funds. LPs typically include pension funds, university endowments, sovereign wealth funds, insurance companies, foundations, and high-net-worth individuals or family offices. They invest in VC funds seeking diversified exposure to high-growth private companies and superior returns that often outperform traditional asset classes over the long term. LPs typically have limited liability, meaning their financial risk is capped at their initial investment, and they have no direct involvement in the day-to-day investment decisions of the fund. Their primary role is to provide the capital that venture capitalists then deploy.

General Partners (GPs): The Fund Managers (Venture Capitalists)

The General Partners (GPs) are the venture capitalists themselves – the individuals or teams who manage the venture capital fund. They are responsible for raising capital from LPs, identifying promising startups, conducting due diligence, negotiating deals, and actively managing the portfolio companies. GPs put their reputation and often a significant portion of their own capital at risk, aligning their interests with both the LPs and the founders they invest in. They typically earn money in two ways: through a management fee (usually 2% of the fund’s committed capital annually, covering operational costs) and through a share of the profits, known as “carried interest” (typically 20-30% of the profits generated from successful investments). GPs are the engine of the VC ecosystem, bringing expertise, networks, and strategic guidance to their portfolio companies.

Venture Capital Firms: The Investment Vehicles

A Venture Capital Firm is the entity that houses the GPs and manages the VC funds. These firms range from boutique operations to large, multi-stage global players. Each firm typically has a specific investment thesis, focusing on particular industries (e.g., SaaS, biotech, fintech), stages of development (seed, Series A), or geographic regions. Examples include Sequoia Capital, Andreessen Horowitz, and Accel. These firms are critical for their ability to source deals, conduct rigorous analysis, and provide post-investment support. They often have dedicated teams for market research, deal sourcing, legal, and operational support, all aimed at maximizing the success of their portfolio companies.

Founders & Startups: The Innovators

At the core of the VC ecosystem are the Founders and Startups – the entrepreneurs with innovative ideas, disruptive technologies, and the ambition to build significant businesses. These are the companies that seek venture capital to fund their growth, product development, market expansion, and talent acquisition. For a startup, securing VC funding is not just about the money; it’s also about gaining credibility, accessing the VC firm’s network of advisors and potential customers, and benefiting from the strategic guidance of experienced investors. Founders need to meticulously craft their pitches, demonstrate market traction, and articulate a clear vision for growth to attract VC attention.

Angel Investors: Early-Stage Fuel

While distinct from VC firms, Angel Investors are crucial early-stage players. These are affluent individuals who invest their personal capital directly into startups, often at the seed or pre-seed stage, usually in exchange for equity. Angels often provide the very first capital a startup receives, bridging the gap before institutional VCs come into play. They typically invest smaller amounts than VC firms, but their early belief and capital can be instrumental in getting a startup off the ground. Many successful VC-backed companies began with angel funding, making angels an indispensable part of the broader startup funding landscape.

Understanding the interplay between these different players is key to navigating the venture capital world. LPs provide the fuel, GPs drive the vehicle, and founders are the innovators charting the course, all within a structured environment designed to foster high-growth companies.

The Venture Capital Funding Stages: A Journey of Growth

1. Pre-Seed Stage: The Genesis

The Pre-Seed stage is the earliest phase, often before a company is even formally incorporated. Funding at this stage usually comes from founders’ personal savings, friends and family, small grants, or angel investors. The capital is used to validate an idea, build a minimum viable product (MVP), conduct market research, and assemble an initial team. Valuations are typically low, and the investment is highly speculative, based mostly on the team and the nascent idea. For instance, a startup in this phase might be experimenting with different tech stacks to find the most efficient way to build their core product, or rigorously researching their target audience.

2. Seed Stage: Nurturing the Sapling

The Seed stage marks a company’s transition from an idea to a tangible product or service with some initial traction. Seed funding, usually ranging from a few hundred thousand to a few million dollars, helps companies refine their product, acquire their first users or customers, and build out their core team. Investors at this stage, often angel groups or dedicated seed funds, look for a strong team, a large addressable market, a defensible product vision, and early indicators of product-market fit. The goal is to prove the business concept and prepare for more substantial institutional investment. Project management becomes critical here; early-stage startups often leverage lightweight, agile project management software startups to keep development on track and manage resources efficiently.

3. Series A: Scaling the Vision

Series A is often the first significant institutional round of funding, typically led by venture capital firms. Companies raising a Series A have usually achieved significant product-market fit, demonstrated consistent revenue or user growth, and have a clear strategy for scaling. The capital (typically $2 million to $15 million, but often higher in 2026) is used to scale operations, expand into new markets, hire key talent, and further develop the product. VCs at this stage meticulously evaluate the business model, unit economics, team, and market opportunity. A strong narrative, backed by data, is essential, and understanding how to articulate your vision, much like how to write blog posts that rank on Google, applies to pitching to VCs – clarity, authority, and value proposition are paramount.

4. Series B & Beyond: Accelerating Growth

Following a successful Series A, companies typically enter Series B, C, D, and subsequent growth rounds. Each successive round injects more capital, usually in larger amounts ($10 million to hundreds of millions), to fuel aggressive expansion. At these stages, companies are expected to have robust revenue streams, established market positions, and proven scalability. Capital is deployed for international expansion, strategic acquisitions, entering new product lines, and fending off competitors. Investors at these later stages look for sustained growth, strong leadership, and a clear path to profitability or market dominance. Valuations increase significantly with each round, reflecting the reduced risk and increased market validation.

5. Growth Equity / Pre-IPO Stage: Nearing the Summit

The Growth Equity or Pre-IPO stage is for very mature private companies that are nearing an exit event, such as an Initial Public Offering (IPO) or a major acquisition. These companies are typically generating substantial revenue, may be profitable, and are looking for capital to consolidate their market position, make strategic investments, or provide liquidity to early investors and employees. Growth equity investors often take smaller, non-controlling stakes compared to early-stage VCs, focusing on companies with a clear trajectory to becoming public entities or major acquisition targets. This stage bridges the gap between private and public markets, setting the stage for the company’s ultimate venture capital exit.

Each funding stage represents a new chapter in a startup’s life, requiring different strategic priorities, financial targets, and investor expectations. Founders must meticulously prepare for each round, understanding that the journey through these stages is a marathon, not a sprint, demanding continuous innovation, execution, and adaptation.

How Venture Capital Works: The Investment Process Explained

The process by which venture capital firms identify, invest in, and nurture startups is a structured, often lengthy, and highly competitive journey. It involves several distinct phases, from initial contact to eventual exit, each with its own set of challenges and objectives. Understanding this intricate process is key for both aspiring founders and those looking to grasp the mechanics of the VC industry.

1. Deal Sourcing and Screening: Finding the Gems

The first step in how venture capital works is deal sourcing. VC firms actively seek out promising startups through various channels: referrals from their network (other founders, LPs, advisors), incubators and accelerators, industry conferences, pitch events, and increasingly, inbound applications or cold outreach. GPs and their teams spend considerable time networking and building relationships to identify companies that align with their investment thesis. Once potential deals are identified, they undergo an initial screening process. This involves a quick review of the pitch deck, executive summary, and initial data to determine if the startup meets the firm’s basic criteria regarding market size, team experience, product innovation, and traction. Many opportunities are filtered out at this early stage.

2. Initial Meetings and Deeper Dive: Building Relationships

If a startup passes the initial screening, the VC firm will request more detailed information and arrange initial meetings with the founders. These meetings are crucial for both sides to assess fit. VCs aim to understand the team’s vision, capabilities, and resilience, while founders evaluate the VC firm’s potential value beyond capital. This phase often involves multiple conversations, product demonstrations, and a deeper exploration of the business model, market opportunity, and competitive landscape. The VC team will begin to form an opinion on the startup’s potential, often comparing it against their existing portfolio and market trends. They might delve into the specifics of a company’s technology, asking questions about what is a tech stack and how to choose the right one for scalability and future innovation.

3. Due Diligence: The Scrutiny Phase

For startups that progress, the due diligence phase begins. This is a rigorous, comprehensive investigation into every aspect of the company. VC firms will examine financial records, legal documents, intellectual property, customer contracts, employee agreements, market analysis, technology assessments, and competitive positioning. They will talk to customers, former employees, and industry experts. The goal is to uncover any potential risks, validate the founders’ claims, and assess the true potential and defensibility of the business. This process can be intense and time-consuming for founders, requiring transparency and meticulous record-keeping. A well-prepared startup, with clear financials and a strong legal foundation, can significantly streamline this phase.

4. Term Sheet and Negotiation: Defining the Deal

If due diligence is successful and the VC firm decides to invest, they will issue a term sheet. This non-binding document outlines the key terms and conditions of the investment, including the valuation of the company, the amount of capital to be invested, the type of securities (e.g., preferred stock), board representation, liquidation preferences, anti-dilution provisions, and other protective clauses for the investors. Negotiation ensues, where founders, often advised by legal counsel, work to secure the most favorable terms possible. This stage requires a deep understanding of financial and legal implications, as these terms will govern the relationship between investors and founders for years to come.

5. Investment and Post-Investment Support: Beyond the Check

Once the term sheet is finalized and legal documents are signed, the investment is made. However, how venture capital works doesn’t stop at writing a check. Post-investment, VC firms typically become active partners. This often includes taking a board seat, providing strategic guidance, helping with key hires, making introductions to potential customers or partners, and assisting with follow-on fundraising rounds. VCs leverage their extensive networks and experience to help portfolio companies navigate challenges and capitalize on opportunities. They monitor performance closely, often requiring regular updates and reporting, and apply pressure for rapid growth and execution. This active involvement is a significant differentiator of VC funding and a major value-add for startups.

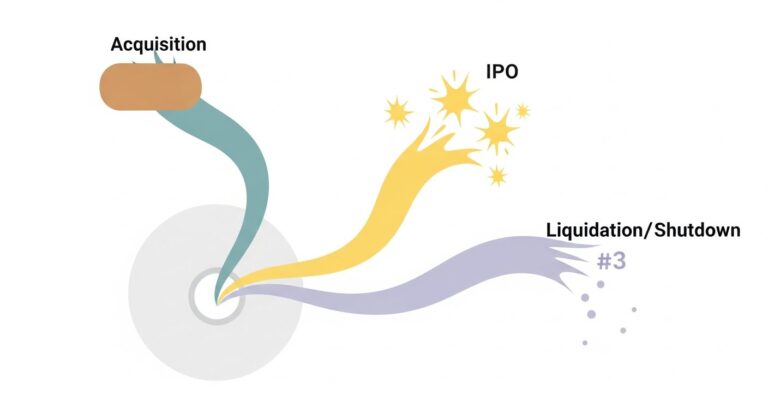

6. Exit Strategies: Realizing Returns

The ultimate goal for a VC investment is a profitable exit, which allows the VC firm to return capital to its LPs and realize its own carried interest. The most common exit strategies include:

- Acquisition (M&A): The startup is bought by a larger company, often a strategic corporate buyer looking to integrate the startup’s technology, talent, or market share. This is the most frequent exit for VC-backed companies.

- Initial Public Offering (IPO): The startup goes public, offering its shares on a stock exchange. This is typically reserved for very large, successful companies with significant revenue and growth potential. IPOs provide high visibility and liquidity but are less common than acquisitions.

- Secondary Sale: Early investors or founders sell their shares to another investor (e.g., a later-stage VC firm, private equity firm, or hedge fund) before an IPO or acquisition.

The exit process can take many years, often 5-10 years or more from the initial investment. The success of these exits is what drives the entire venture capital ecosystem, creating a cyclical flow of capital and innovation. Understanding the full lifecycle, from sourcing to exit, provides a comprehensive view of how venture capital truly works and its profound impact on the startup world.

The Benefits and Risks of Venture Capital for Startups

For an ambitious startup, securing venture capital can feel like winning the lottery – a golden ticket to accelerated growth and market dominance. However, like any powerful tool, VC funding comes with both significant advantages and considerable drawbacks. Founders must carefully weigh these benefits against the inherent risks before embarking on the venture capital journey.

Benefits of Venture Capital

- Significant Capital for Rapid Growth: The most obvious benefit is access to substantial funding that can fuel aggressive hiring, product development, marketing campaigns, and market expansion. This capital allows startups to scale much faster than they could with bootstrapping or traditional loans, enabling them to seize market opportunities quickly and establish a competitive edge. For a startup needing to scale its digital marketing efforts, for example, VC funding can provide the budget to hire a team of content strategists and SEO specialists, enabling them to apply principles like how to write blog posts that rank on Google at a much larger scale.

- Strategic Guidance and Expertise: VCs bring more than just money to the table. General Partners (GPs) often have deep industry experience, a track record of building successful companies, and a keen understanding of market dynamics. They provide invaluable strategic advice, mentorship, and operational guidance, helping founders navigate complex challenges, make critical decisions, and avoid common pitfalls. This expertise can be particularly beneficial in areas like business model refinement, talent acquisition, and scaling operations effectively, perhaps even advising on the optimal use of best project management software for startups to manage rapid growth.

- Access to a Powerful Network: Venture capital firms have extensive networks that can open doors to key customers, strategic partners, potential acquirers, and top-tier talent. They can introduce founders to industry leaders, advisors, and follow-on investors, significantly accelerating business development and fundraising efforts. This network effect alone can be a game-changer for a young company.

- Credibility and Validation: Securing investment from a reputable VC firm is a powerful signal of validation for a startup. It enhances credibility with potential customers, partners, and future employees, making it easier to attract talent and forge strategic alliances. It signifies that experienced investors believe in the company’s vision and potential.

- Structured Growth and Accountability: While sometimes perceived as pressure, the accountability that comes with VC funding can be a significant benefit. VCs often demand rigorous reporting, clear milestones, and disciplined execution. This structured approach can instill greater operational rigor and focus, pushing companies to achieve ambitious targets and maintain a high level of performance.

Risks of Venture Capital

- Dilution of Ownership: The most significant risk is equity dilution. In exchange for capital, founders give up a percentage of ownership in their company. With each successive funding round, their ownership stake decreases. While a smaller slice of a much larger pie can be more valuable than a large slice of a small pie, founders must be prepared for reduced control and a smaller share of the eventual profits.

- Loss of Control and Board Influence: VCs typically take board seats and often have significant influence over strategic decisions, hiring, and even potential exit opportunities. While their input is often beneficial, it means founders may have to compromise on their original vision or strategic direction. Disagreements with board members can lead to tension and even the replacement of founders.

- Pressure for Rapid Growth and High Returns: Venture capital is designed for exponential growth. VCs expect significant returns on their investments (often 10x or more), which translates into immense pressure on startups to achieve aggressive milestones and scale rapidly. This intense pressure can lead to burnout, hasty decisions, and a focus on growth at all costs, potentially sacrificing long-term sustainability or company culture.

- Demanding Exit Expectations: VCs invest with an exit in mind. This means founders might be pushed towards an IPO or acquisition that may not align with their preferred timeline or strategic objectives. The company’s future might be dictated by the investors’ need to achieve a return on their capital within a certain timeframe.

- Time-Consuming Fundraising Process: The process of raising venture capital is incredibly time-consuming, diverting founders’ attention away from building the product and managing the business. From deal sourcing to due diligence and negotiation, it can take months, sometimes even over a year, to close a funding round.

- Misalignment of Interests: Despite best intentions, sometimes the interests of founders and VCs can diverge. For example, founders might prefer a slower, more sustainable growth path, while VCs might push for a rapid, high-risk expansion. Disagreements over valuation, exit timing, or strategic direction can strain relationships.

Ultimately, the decision to pursue venture capital is a strategic one. For companies with massive market potential, a strong team, and a clear path to disruption, the benefits often outweigh the risks. However, founders must enter the process with open eyes, understanding the trade-offs involved and being prepared for the intense demands that come with accepting VC funding.

Is Venture Capital Right for Your Startup in 2026?

Deciding whether to pursue venture capital funding is one of the most critical strategic choices an entrepreneur will make. It’s not a universal solution for every startup, and in 2026, with evolving market dynamics, technology landscapes, and investor preferences, this decision requires even more careful consideration. To determine if venture capital is the right path for your venture, you need to assess your company’s characteristics, market potential, and long-term aspirations.

What VCs Look For in 2026

Venture capitalists are selective, and their criteria are often stringent. In 2026, beyond the foundational elements, VCs are increasingly scrutinizing certain aspects:

- Massive Market Opportunity: VCs seek companies addressing large, growing, or untapped markets where they can achieve significant scale. They want to see a clear path to becoming a market leader, not just a niche player.

- Exceptional Team: This is often the most critical factor. VCs invest in founders with a strong vision, relevant experience, complementary skill sets, resilience, and the ability to execute. They look for passion, integrity, and a deep understanding of their industry.

- Innovative Product/Technology: Your offering must solve a significant problem, be differentiated from competitors, and ideally have a defensible advantage (e.g., proprietary technology, network effects, strong brand). VCs will certainly be asking about your tech stack and how you chose it to support scalability and future innovation.

- Strong Traction and Metrics: While early-stage companies might have less, VCs look for evidence of product-market fit. This could be rapid user growth, recurring revenue, strong engagement metrics, positive customer feedback, or strategic partnerships. Data-driven insights are paramount.

- Clear Business Model and Path to Profitability: How will your company make money? VCs want to understand your revenue streams, unit economics, and a credible path to sustainable profitability, even if it’s years down the line.

- Defensibility and Moat: Can your business withstand competition? VCs look for “moats” – competitive advantages that make it difficult for others to replicate your success. This could be intellectual property, brand loyalty, proprietary data, or economies of scale.

- Scalability: Your business model must be inherently scalable, capable of growing exponentially without a proportional increase in costs. Software-as-a-Service (SaaS) and platform businesses are often favored due to their high scalability.

- Alignment with VC Thesis: Each VC firm has a specific investment thesis (industry focus, stage preference, geographic region). Ensure your company aligns with what a particular firm typically invests in.

- ESG Considerations: Increasingly, VCs are also factoring in Environmental, Social, and Governance (ESG) criteria, looking for companies with sustainable practices and positive societal impact, especially those targeting younger generations who prioritize these values.

When VC Might Be Right for You

Venture capital is most suitable for startups that:

- Have a “Unicorn” Ambition: You aim to build a multi-billion dollar company that will disrupt an industry, not just a lifestyle business.

- Operate in a High-Growth Market: Your market segment has massive potential for expansion and innovation.

- Require Significant Capital for Rapid Scaling: Your business model necessitates large investments in R&D, talent, or market penetration to achieve dominance quickly.

- Possess a Strong, Experienced Team: You have a founding team with a proven track record or unique expertise.

- Are Willing to Dilute Ownership: You understand and accept that giving up equity and some control is a necessary trade-off for accelerated growth.

- Are Open to Active Investor Involvement: You welcome strategic guidance, board participation, and the demands that come with active investors.

Alternatives to Venture Capital

If your startup doesn’t fit the VC profile or if you prefer a different growth trajectory, several alternatives exist:

- Bootstrapping: Funding your business through personal savings, early customer revenue, and minimal external capital. This maximizes ownership and control but limits growth speed.

- Angel Investors: High-net-worth individuals who invest their own money, often at earlier stages than VCs. They can be less demanding than institutional VCs but typically invest smaller amounts.

- Debt Financing: Loans from banks or other financial institutions. This avoids equity dilution but requires collateral and predictable cash flow, often unsuitable for early-stage, high-risk startups.

- Grants: Non-dilutive funding from government agencies, foundations, or corporations, often tied to specific research or social impact goals.

- Crowdfunding: Raising small amounts of capital from a large number of individuals, either through equity (giving up small stakes) or rewards (pre-selling products).

- Incubators and Accelerators: Programs that provide initial capital (often convertible notes), mentorship, and resources in exchange for a small equity stake, helping prepare startups for larger funding rounds.

In 2026, the venture capital landscape continues to be competitive and dynamic. While it offers unparalleled opportunities for rapid scaling and market disruption, it also demands immense commitment, a willingness to share control, and an unyielding focus on aggressive growth. Evaluate your startup’s potential, your personal goals, and the market context thoroughly to make an informed decision about whether venture capital is the right fuel for your entrepreneurial engine.

Frequently Asked Questions About Venture Capital

What is the typical return VCs expect on their investments?

Venture capitalists typically aim for very high returns to compensate for the high risk associated with early-stage investments. While there’s no single number, VCs often look for companies with the potential to generate 10x or even 20x returns on their investment within a 5-10 year timeframe. This is because a significant portion of their portfolio companies will fail or provide only modest returns, so a few “home run” investments need to cover those losses and deliver overall fund performance that satisfies their Limited Partners (LPs).

How long does it take to raise venture capital?

The venture capital fundraising process can be lengthy and varies significantly based on the stage of funding, market conditions, and the startup’s readiness. For a seed or Series A round, it typically takes anywhere from 3 to 9 months from initial outreach to closing the deal. This includes several stages: initial meetings, deeper dives, extensive due diligence, term sheet negotiation, and legal finalization. Founders should factor this time commitment into their operational planning and ideally start fundraising before they desperately need the capital.

Can a startup raise venture capital without a finished product?

Yes, especially at the pre-seed and seed stages. Many venture capital firms and angel investors are willing to invest in startups that have a strong concept, a compelling vision, a well-researched market opportunity, and most importantly, an exceptional team. While having a Minimum Viable Product (MVP) or early prototypes with some user traction is always beneficial and increases the chances of securing funding, it’s not always a prerequisite. Investors often bet on the team’s ability to execute and build the product after receiving the investment.

What is a “unicorn” in venture capital?

In venture capital, a “unicorn” is a privately held startup company with a valuation exceeding $1 billion. The term was coined in 2013 by Aileen Lee, founder of Cowboy Ventures, to highlight the rarity of such successful startups. Examples include companies like SpaceX, Stripe, and formerly Airbnb or Uber before their IPOs. Achieving unicorn status is a significant milestone that signifies immense growth, market disruption, and substantial investor returns.

What is a “due diligence” process in VC?

Due diligence is a comprehensive investigation and audit performed by a venture capital firm before making an investment. It involves a thorough examination of a startup’s financials, legal documents, intellectual property, market, technology, team, customer base, and operational processes. The goal is to verify all claims made by the founders, identify any potential risks or liabilities, and confirm the business’s viability and growth potential. This rigorous process helps VCs make informed investment decisions and mitigate risk.

Do VCs always take a board seat?

Not always, but it’s very common, especially in later-stage rounds (Series A, B, and beyond). At the seed stage, VCs might opt for an observer seat (attending board

Recommended Resources

Explore Time Blocking Method How To Use It for additional insights.

You might also enjoy How To Choose The Right Font Pairing from Layout Scene.